👉(12 Executive Actions) Opportunities in the new higher-for-longer world - Fewer rate cuts in 2024

💡 Exclusive Macro & Business Insights

Thanks for reading!!!

📌 As my subscriber you get totally FREE my Exclusive Premium Insights that I do and share only with you.

You won't find these materials shared by me on any other platform.

By subscribing you’ll join over 500 people who read Macro & Business Insights weekly!

(12 Executive Actions) 👇

ONE MORE RATE HIKE LEFT ON THE TABLE, RATE CUT FORECAST REDUCED IN 2024 🔔

(1) 🚨 “The key focus area for investors was the update to the "dot plot," or the FOMC's best estimate of where it sees the path of interest rates going.”

(2)✔ “The median dot for 2023 remained at 5.6%, which implies perhaps one more rate hike is on the table, while the rest of the dots for 2024 - 2026 all shifted higher.”

(3)✔ “The Fed pulled back its estimate of rate cuts in 2024 from 100 basis points (1.0%) of cuts to just 50 basis points, although cuts in 2025 are still expected to be 120 basis points, followed by another 100 basis points in 2026, bringing the fed funds rate to under 3.0%.”

FED’S NEXT MOVE

(4)✔ “The Fed's next move may depend more on the trajectory of the economy.”

(5)✔ “While it now forecasts stronger growth in 2023 and 2024, if the consumer or broader economy does weaken, the Fed may decide to cut rates sooner or more than by just 50 basis points next year.”

(6)✔ “If growth holds up and inflation continues to gradually ease, then we think the market's current view is credible, and over time the Fed will steadily normalize rates down toward a neutral level.”

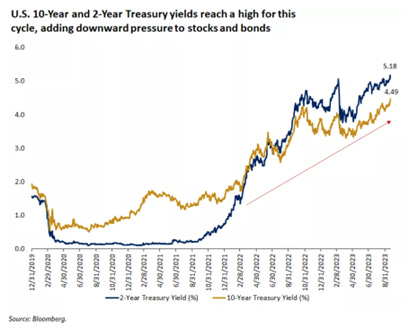

YIELDS MOVE HIGHER, AND STOCKS MOVE LOWER

(7)✔ “The primary reaction in markets has been an outsized move higher in Treasury yields and a swift move lower in stocks.”

(8)✔ “With both the 2-year and 10-year U.S. Treasury yields hitting highs of this cycle after the Fed meeting, longer-duration parts of both fixed-income and equity markets have been the laggards in recent days.”

(9)✔ “Historically, a rapid rise in yields has weighed particularly on higher valuation growth parts of the market, and this could continue in the near term.”

(10)✔ “For equities, the higher yields also come at a time when there was some concern around extended valuations, particularly in the large-cap technology space and among the "Magnificent 7" (Magnificent 7 stocks include AAPL, AMZN, GOOGL, META, MSFT, NVDA, TSLA).”

Opportunities in the new higher-for-longer world

(11)✔ “How should investors think about portfolios in this new "higher for longer" regime? While higher rates can put pressure on parts of the stock and bond market, they can also create opportunities for certain segments leveraged to higher yields.”

EQUITIES: we would expect some broadening in leadership to emerge as rates remain elevated, and investors could look to complement growth and technology sectors with parts of the market that have more favorable valuations.”

(12)✔ “Over time, cyclical sectors, like industrials and materials, and even small-cap and international stocks, may play some catch-up.”

BONDS: historically, one of the best predictors of forward returns is current yields, and if the Fed is indicating it is close to a peak interest rate, this could be a favorable time for high-quality bonds. Not only do you lock-in better rates for longer, but you have the chance for price appreciation if and when the Fed pivots lower as well.

📢 Surely if I had had someone to explain or teach me these 10 lessons at the beginning, just as I’m now doing with you, I surely would have avoided making a lot of mistakes.

⚡ This definitive completed guide is totally free - and for receive it the only thing I ask you in return is to bring just 1 passionate people like you into our community with the link below 🙏👇👇👇

💌 Sign up to my weekly email newsletter

🎙 PODCAST

Best regards,

Ale

Disclosure

This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. This material has been prepared for informational purposes only. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.